New York’s annual legislative session ends Wednesday. And that means, predictably, a mad rush to get legislation enacted without having to wait another year. Or, conversely, a mad rush to stop legislation.

And that’s where we are today, with Geico attempting to halt legislation that would hold it (and other insurance companies) accountable for bad faith in settlement negotiations. Yes, out-of-state-readers, it’s true, New York currently has very limited ways to stop insurance companies from trying to screw you over in your time of distress.

This legislation was first proposed in the wind-swept wake of Hurricane Sandy in 2013, when insurance companies thought it would be a really cool idea to deny coverage for damaged homes. If a policy excluded wind damage, the insurers would claim water was to blame. If it excluded water damage, they would claim wind was to blame.

The denials had a common background – they were dealing with people who had their homes destroyed and were, therefore, in great economic distress. Because everyone needs a roof over their heads. So the denials gave the insurance companies some, let’s call it, leverage.

Delay and delay and force the homeowners to hire lawyers to sue. Then, when the pain is deep enough and the homeowners desperate enough, maybe settle for 50 cents on the dollar. Or 70. But even if the insurers had to cough up 100 cents on the dollar on some claims, so what? That was merely what they had to do anyway. Every cent saved was profit.

And that is part of the base model of the insurance company: Take in as much as you can in premiums and pay out as little as possible and invest the money in the interim.

The legislation that is proposed, that Geico is afraid of, would put a stop to that as well as bad faith tactics in auto policies and elsewhere.

Right now, in an auto case, if an insurance policy is only the bare minimum $25,000 or maybe $100,000, and the damages are $500,000, the insurance company has a vested interest in offering only a portion of the policy. Sure, it’s possible that someone will spend $20,000 and try the case to verdict. But that often makes little economic sense, and all the lawyers know it. You can win but still lose. So why offer the whole policy even if you would, in good faith, owe it?

The only avenue for relief currently is to take an excess verdict against the insured when the insurance company has elected to put its own interests ahead of those customers, because you can’t sue the insurance company directly.

And then, and only then, if the insured is smacked for a big, fat verdict in excess of the insurance policy, there might be some relief. But that relief only comes if the defendants — who you just sued and perhaps, inflicted a bit of anxiety on — then assign their own rights to sue the insurance company for bad faith back to the people that had sued them. And if those people are gone? Or say “screw you, we don’t feel like helping you as we got nothing to take anyway so it doesn’t matter to us?” Well, sorry Charlie.

The bad faith legislation that is now pending would fix this problem, a problem created by the fact they are currently required to act in good faith but there is only one very poor method of enforcement.

Enter, stage right, Geico to oppose this common-sense legislation. In a mass email yesterday from Rick Hoagland, a Geico senior vice president, to its policy holders, it urges people to call their legislators to stop the legislation and protect the insurance company profits.

OK, maybe Hoagland didn’t word it quite that way. He claimed, instead, that legislation protecting both policy holders and the people they may injure would somehow be bad for them. George Orwell would have been proud.

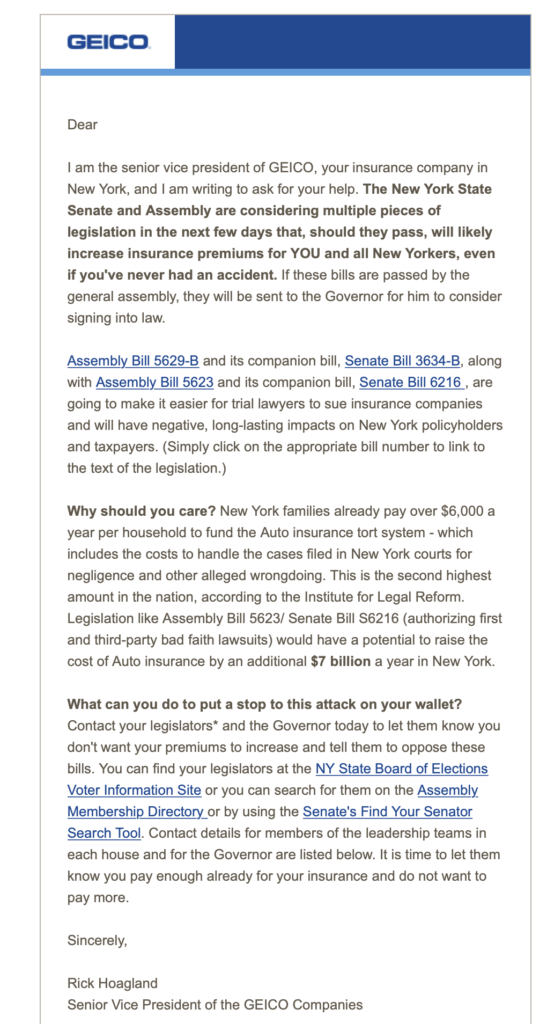

He writes, instead that:

I am the senior vice president of GEICO, your insurance company in New York, and I am writing to ask for your help. The New York State Senate and Assembly are considering multiple pieces of legislation in the next few days that, should they pass, will likely increase insurance premiums for YOU and all New Yorkers, even if you’ve never had an accident.

He doesn’t say it would increase premiums but rather, he speculates. He provides no empirical data. More importantly, he doesn’t tell his insured that the legislation protects them from the bad faith practices of Geico, the company that they paid money to in order to protect them in the event something goes awry. And it is those bad faith practices that could put their own homes at risk in the event of a verdict in excess of their insurance policies.

And, of course he doesn’t tell his readers that the bills are designed to protect them. No, he claims that they “make it easier for trial lawyers to sue insurance companies.”

Here’s an idea, why not just put us personal injury lawyers out of business by dealing in good faith to begin with? Look, Geico I solved your problem! (You’re welcome. No charge.)

Here’s the Geico pitch, compete with links to the bills, which I urge people to read so the they know they are consumer protection bills. The reason he provided links is because he knew, no doubt, that few people would actually click them or get an explanation as to their true purpose:

Assembly Bill 5629-B and its companion bill, Senate Bill 3634-B, along with Assembly Bill 5623 and its companion bill, Senate Bill 6216 , are going to make it easier for trial lawyers to sue insurance companies and will have negative, long-lasting impacts on New York policyholders and taxpayers. (Simply click on the appropriate bill number to link to the text of the legislation.)

The legislation would allow a direct case against the insurance company for bad faith, so that the victims don’t have to rely upon the people they just sued to tender their rights against the insurers.

Geico, of course, would like to make enforcement of good faith laws difficult, thereby giving it a certain level of immunity. Why not offer 20K on a 25K policy when you know it will cost the injured plaintiff that much just to try the case? There’s almost no downside for them for acting in bad faith.

It’s time New York finally put a stop, once and for all, to the bad faith of insurance companies. The law requires good faith dealing and the Legislature should give consumes the tools to enforce it.

The email is here:

Of course, GEICO is against it. Killing the legislation keeps the liability for bad faith on insurance company customers rather than the insurance company. We are taking almost every case to trial now where the insurance company doesn’t offer a fair settlement and will go after their customers’ personal assets and income. Insurance companies don’t like the bad publicity that creates when they’re trying to sell insurance.

We even recently refused an insurance company offer of the entire $25,000 policy because they would not pay the property damage for our client’s motorcycle. The insurance company could not understand why we would not accept payment of the policy. We started a lawsuit for personal injuries and property damage and litigated for several months over a few thousand dollars of property damage to the motorcycle. The insurance company gave in and paid the property damage. We didn’t even charge our client a legal fee for the property damage.

If the insurance company would not have paid the property damage, we would have taken the case to trial and gotten a substantial verdict for the injuries.

At this point in my career, my only interest is making insurance companies miserable.

By the way, thank you for your article! You have one of the best blogs on the Internet.

Thank you.

Came here years ago for Rafalski vs. The Internet,

Still here today because of posts like this.

Eric Turkewitz is one of the few people speaking online that are genuinely worthy of your attention, whatever he has to say.

Their misleading and alarmist e-mail is proof of why we can’t trust insurance companies to do the right thing by their customers. We need to hold insurance companies accountable for their bad faith now!

Interesting perspective from the white-horse-plaintiff attorney side. What you’re saying makes some sense, of course, but you’re omitting the potential real-world application of these “consumer protection” bills (which suspiciously didn’t make it to the Legislature until it fell under Democratic [aka plaintiff’s attorney lobbying money recipient]) control).

You use hurricane victims as an example, and there should be no debate that what some insurers have done in those scenarios have been despicable. There, however, you’re talking about potentially life-altering sums of money – the replacement value of a home, for example. It’s certainly worth litigating when you have the potential to recover hundreds of thousands of dollars after the carrier disclaims on groan-inducing grounds.

Of course, the bills go well beyond that sympathetic scenario. AB 5629-B provides, in relevant part:

“against the insurer to recover damages including compensatory damages and interest measured from the time of failure to offer a fair and reasonable settlement from such insurer to the full extent of the judgment against the insured, not limited to the policy limits”

Therein lies the rub: if the carrier fails to offer a “fair and reasonable settlement” (to be determined, by a preponderance of the evidence, by pro-plaintiff Bronx/Kings/Queens County juries that routinely hand out massive verdicts for specious claims, and affirmed by the Appellate Division, which is increasingly staffed with former Bronx/Kings/Queens judges thanks to 13 years of single-party governorship), and the plaintiff scores a windfall, they can sue the carrier and recover IN EXCESS OF THE POLICY LIMITS.

The immediate effect of this, once it has taken effect and a few carriers have been made an example of, will be that insurers will simply tender the full value of low-end policies anytime the damages threaten to exceed their limits. Congratulations, plaintiff’s bar, now you’ll get the full $25k auto policy once your client has seen one of the chop-shop orthopedists that you have on speed dial, instead of having to litigate over that last few thousand. A windfall for your average Court Street attorney, thought it probably won’t help the average Joe who now has to pay 10% more for his bare-bones $25k auto policy. Better call The General, Joe!

At the higher end, however, things will get dicier. There is ample precedent that a single orthopedic surgery can have a sustainable verdict value of $1,000,000 or more for pain and suffering alone. Ask one of the big PI firms that hand out swag to construction workers how much that turns into once you add union benefits.

So, fall off a ladder.. because it… “moved” (or claim you did, when no one was around to say otherwise – but I digress), finally get that ‘ole partial meniscus tear from few years before fixed up, and leverage the carrier for the policy limits right off the bat. They should know, after all, how much an ambulatory surgery is worth in New York! And if they don’t offer it? Try the case, and go after the carrier for every dollar (plus 9% interest!) awarded above the $1M per occurrence limit. After all, at the end of the day, they were just too greedy to cough up every last cent of that policy the second another lawyer purchased an Index Number and threw the receipt into their client’s disbursements folder.

Consumer protection, indeed.

I can’t tell if that comment was written by a human or some evil-lawyer-juror comment generator, as it’s so stuffed with nonsense tropes as you meander to and fro well off the topic at hand.

I’ll keep it simple — and actually on topic — there’s currently a law mandating good faith negotiations. It is violated routinely because there is no downside.

This bill provides an enforcement mechanism.

Your point seems to be that insurance companies should be allowed to keep screwing people again and again, as you failed to provide a solution to the problem.

So, https://youtu.be/g4bftQ4xxFc ?

My argument is that the Legislature’s “solution” to what is, admittedly, a problem in some unique situations, goes entirely too far, and is ripe for exploitation. I outlined exactly how to do so, perhaps you can integrate this strategy into your practice.

Want a better solution? I dunno, maybe limit recover to the policy limits plus actual costs? I don’t see why a carrier should have to pay, e.g., $1.5M on on $500k policy just because a jury decides they should have offered up the policy limits from day one. The whole thing smacks of being written by the Trial Lawyers Association.

You’re correct, there are requirements that carriers negotiate in good faith. Bad faith letters to carriers are routinely written by defense attorneys on behalf of clients to pressure them to settle cases (excess carriers write similar letters to GL carriers). But most of the time it’s for the protection of their client against the ridiculous values being given to relatively minor injuries, or because [ed.– irrelevant, off-topic side comment deleted].

My argument is that the Legislature’s “solution” to what is, admittedly, a problem in some unique situations,

For some carries, it is standard operating procedure. Why cough up a 25K or 50K or 100K policy when that is the worst case scenario? If the plaintiff has to pay 20K to try the case, the economics suck.

Want a better solution? I dunno, maybe limit recover to the policy limits plus actual costs?

So, basically, the carriers still have an incentive to act in bad faith.

But most of the time it’s for the protection of their client against the ridiculous values being given to relatively minor injuries

B.S. Judges toss those rare outlier verdicts. And if the trial judge doesn’t do it, the appellate court will. And that system has worked for over 200 years. See:

How New York CapsPersonal Injury Damages

[i]So, basically, the carriers still have an incentive to act in bad faith.[/i]

Some, but considerably less, especially with lager policies. Jerking someone around over 5k that they are clearly owed is one thing, and the legislation would probably be effective at addressing that – it no longer makes sense to take the risk.

But as the numbers climb, risk factors to insurers grow immensely, and begin to run up against the unfortunate realities of our justice system, which I touched on previously.

[quote]B.S. Judges toss those rare outlier verdicts. And if the trial judge doesn’t do it, the appellate court will. And that system has worked for over 200 years. See:

How New York CapsPersonal Injury Damages[/quote]

I’m well aware of how trial judges and the Appellate Division modifies jury awards. That’s why defense attorneys value cases based on sustainable verdict value – what the Appellate Division is sustaining or modifying for similar damages scenarios.

I notice that your article on the topic omits that trial judges and the Appellate Division also RAISE verdicts in a similar fashion if they think that they jury didn’t give away enough money. The pseudo-ceiling is also a pseudo-floor. Which is why a decade-old case involving a single arthroscopic knee surgery set the general rule that one surgery = one million dollars.

Just because an ever-liberalizing judiciary thinks the full value of many small business’ insurance policies is fair compensation for a 3-hour ambulatory surgery doesn’t make it so.

I notice that your article on the topic omits that trial judges and the Appellate Division also RAISE verdicts in a similar fashion if they think that they jury didn’t give away enough money.

If that is what you claim to have noticed then you are a lousy reader.

Or more likely, you simply made assumptions — to fit your own world view — and then formed opinions based on those assumptions, and didn’t read it at all.

It’s called confirmation bias and it runs through-and-through your screeds.

“I don’t see why a carrier should have to pay, e.g., $1.5M on on $500k policy just because a jury decides they should have offered up the policy limits from day one.”

I don’t understand your complaint. If the company is found, by a jury, to have lowballed its estimate of the liabilities *to such an extent* that there is no plausible good-faith reasoning by which they could arrive at their estimate, then why shouldn’t they be penalized? All you have to do to defend yourself against accusations of bad faith is to show your work. If there is a plausible reason to believe that the liability is less than the policy maximum, then it seems to me that it should be easy enough to simply show the math.

On the other hand, if, as you claim, juries routinely award verdicts well in excess of policy maximums, and these verdicts are sustained on appeal, then why isn’t the policy maximum the only possible good-faith estimate of the actual liability? And if juries don’t routinely award verdicts well in excess of policy maximums, then what is the fuss about?

You must work for the despicable insurance company that recently fought a motion for a special preference because our client was at the end of her life expectancy for a bilateral lung transplant. Your company was hoping she would die before her case got to trial. They got their wish.

That was meant for Tom Rice.

Save your emotional arguments for the jury, Phil.

Appreciated your article.

My own experience: Geico’s tactics were despicable. They went to extreme lengths not to pay out on their policy.

Something clearly needs to be done to protect people.